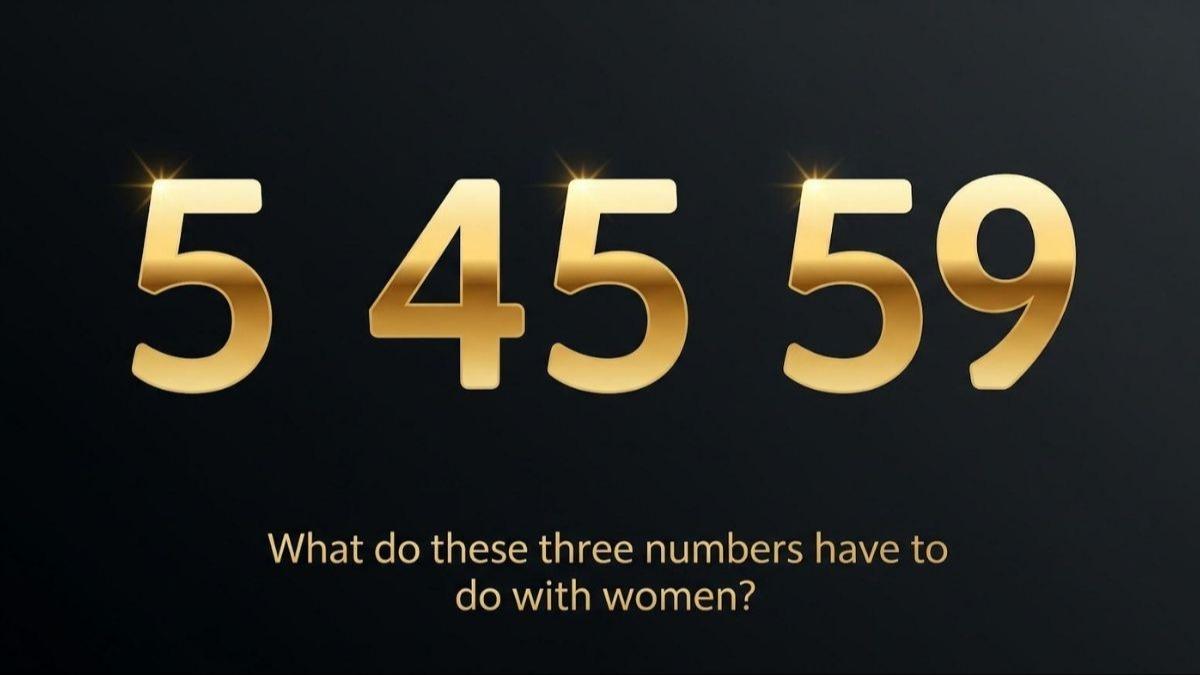

Three Numbers Every Woman Should Know

Key Takeaways

- How much wealth are women on track to control in the next decade, and why does that matter?

- What does the life expectancy gap between women and men mean for how long money needs to last?

- How common is it for women to be primary earners, and how should that change their insurance, investment, and retirement strategy?

- Why does the average age of widowhood, around 59, matter even if it feels “too young” to worry about it?

Why These Three Numbers Matter

A quiet shift is happening. Women are building their own wealth through careers, often serving as the primary earners in their families, and inheriting assets from their parents and spouses. Meanwhile, women are living longer and, in many cases, making financial decisions independently in later life.

The story of women and finance can be told today in three numbers that are shaping many of their lives:

- 5

- 45

- 59

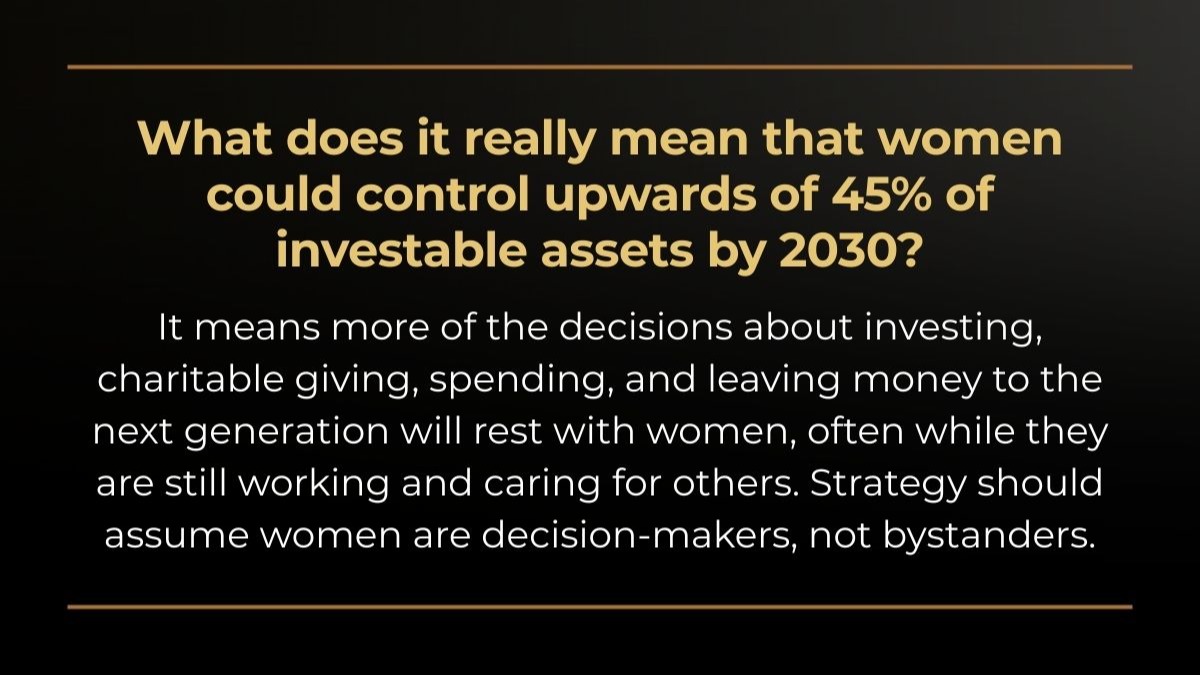

The story these numbers tell is that women are likely to oversee more wealth for longer periods and for more people than previous generations. Financial strategies today should reflect this emerging reality.

#1

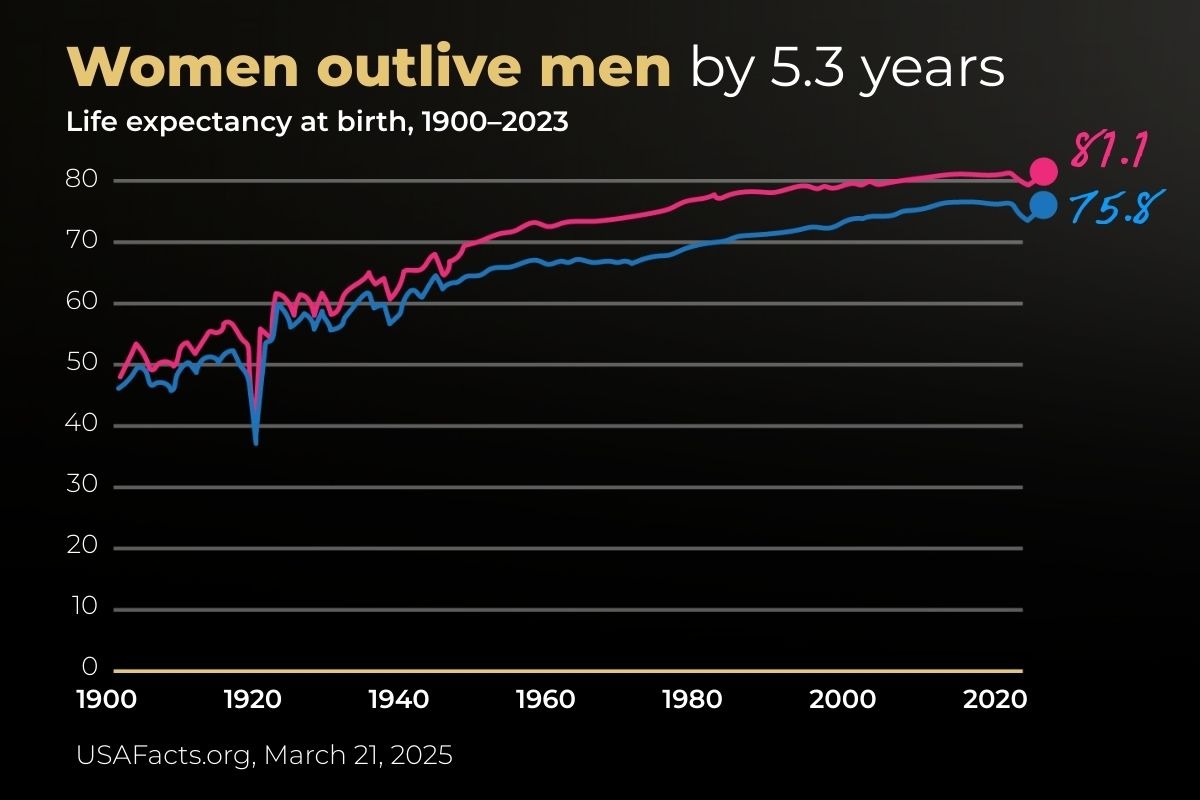

5 - The Extra Years' Money May Need to Last

On average, women in the United States live about five years longer than men. While both men and women are living longer than at the beginning of the last century, a gap remains. In the U.S. in 2023, the life expectancy for men was 75.8 years. For women, it was 81.1 years.1

Other studies highlight that many of those extra years are spent managing health issues. Women, on average, are living longer and also living more years with chronic conditions, which can increase the need for ongoing healthcare and caregiving support.2

While longevity is good news, it has clear financial implications, especially for women. Retirement and investment strategy needs to support:

- A potentially longer time in retirement, possibly 30 years or more.

- Healthcare expenditures may rise as you reach your 70s, 80s, and 90s.

- Periods of reduced work or caregiving, long before traditional retirement, could impact your earnings and asset accumulation.

Are There Financial Considerations That Can Help Support a Longer Life?

Financial strategies should account for the possibility of living longer. When helping our clients create wealth management, retirement income, and estate strategies, life expectancies are always part of the discussion, especially the extra years women are expected to live. Here are three approaches that may be helpful:

- Assume you will be around until at least age 95 on paper, even if you do not expect to live that long; it is much easier to adjust if you have “too much” money late in life than if you have too little.

- Consider separating your portfolio into time horizons: a near-term bucket for the next five to ten years of spending, a longer-term bucket, and a specific healthcare/extended care bucket.

- Stress-test your strategy; discuss with your financial professional historical estimates and simulations of how your strategy may hold up if you live longer than expected, if healthcare costs are higher than average, or if investment returns are lower than the long-term assumptions.

#2

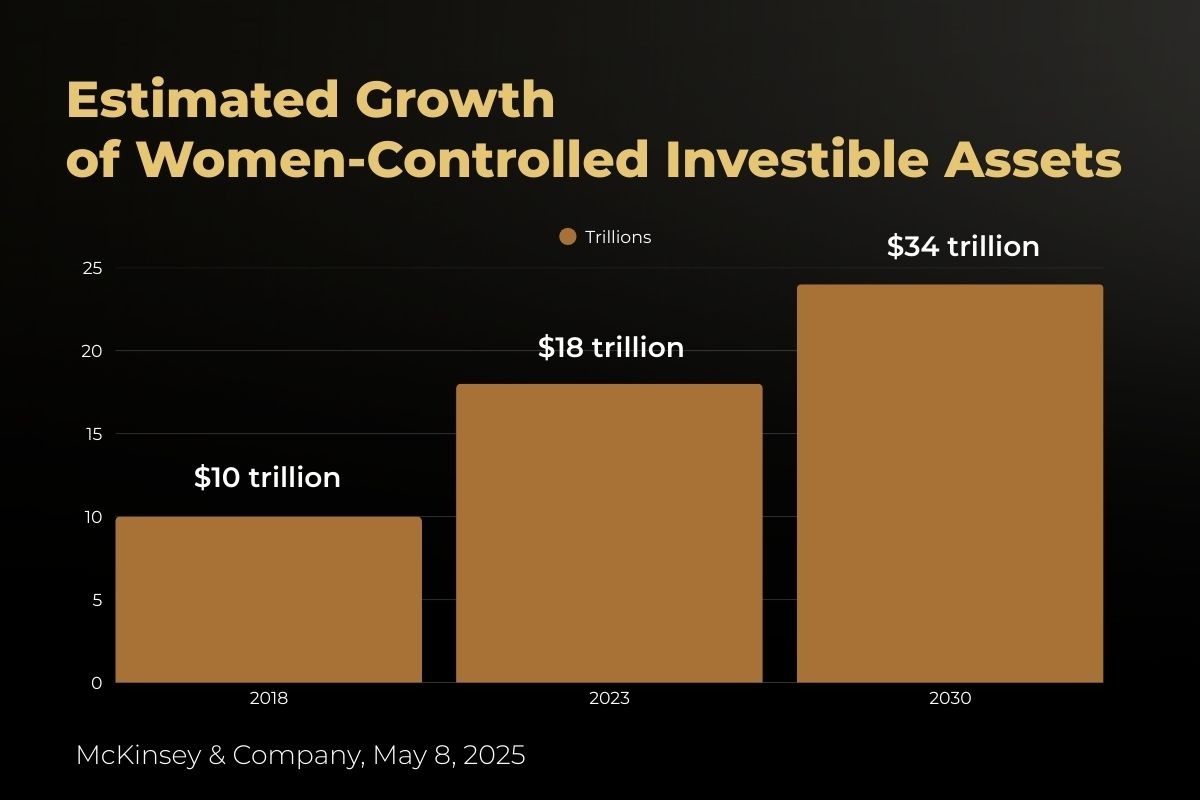

45 - The Share of Investable Assets Women Are on Track to Control by 2030

One study suggested that women may control as much as 45 percent of all investable assets in the U.S. and Europe by 2030.3

This estimated doubling of women-controlled assets is being driven by interrelated social, economic, demographic, and cultural trends. Much of the asset shift is expected to be attributable to the “Great Wealth Transfer” underway from Baby Boomers to younger generations. Some estimates indicate that as much as 70-80 percent of the coming $83 trillion transfer will accrue to women.4

At the same time, income patterns continue to change for women.

- According to the Pew Research Center, 16 percent of opposite-sex marriages had wives as the sole or primary breadwinner, about triple the share from 50 years ago.5

- In 29 percent of marriages, both spouses earn about the same amount of money.5

- In a major change, just over half (55 percent) of marriages have a husband who is the primary or sole breadwinner, down from 85 percent in 1972.5

- In 2023, 45 percent of mothers were breadwinners, either single working mothers or married mothers who earned at least half of their family's income, with another 24 percent considered co-breadwinners.6

Simply put, in today’s world, women are increasingly the ones earning, inheriting, and ultimately directing family wealth. And that shows no signs of changing.

What Does This Mean for Financial Strategy?

For women already managing a portfolio or expecting to inherit one, this trend is not abstract. It raises important questions for both single women and married couples looking to the future. Here are just a few:

- For single women or those who may become widowed, is there a clear, documented investment strategy that reflects their unique goals, time horizons, and comfort with risk, or is there a mix of accounts that grew over time without cohesion?

- If a woman is a primary or co-earner, is the personal finance strategy built around her income, her partner’s income, or both equally?

- Do estate documents and beneficiary designations support the surviving spouse being able to direct wealth to children, charities, and future generations?

What Are Three Financial Strategy Moves to Consider?

As financial professionals, we typically encourage our women clients to consider several approaches to help them pursue their financial and life goals. Here are three:

- Create or update a personal investment policy statement; spell out objectives, time frames, risk guardrails, and how decisions will be made. This is especially important for married couples to discuss in the event that the wife will eventually be the one who stewards the family wealth across generations.

- Consolidate or coordinate scattered accounts; old retirement accounts, inherited assets, and taxable portfolios are easier to quantify, track, and align around a single strategy when consolidated.

- Women who are the primary earners may want to right-size their safety nets by confirming that insurance policies and emergency reserves are built around their income and the people who rely on it.

#3

59 - The Age Many Women Face Widowhood

As financial professionals, we understand that mortality is a difficult yet necessary topic to address, especially for women. While it may be uncomfortable to discuss, married women need to be both emotionally and financially prepared for the distinct possibility that they will outlive their husbands.

What Are Some of the Sobering Facts Around Widowhood?

- The average age of widowhood for women in the United States is 59.7,8

- About 34 percent of women aged 65 and older in the U.S. are widows, rising to 58 percent for women aged 75 and older.

- Nearly 700,000 women lose their husbands each year in the U.S.

- Women live 12-13 years on average as widows.

- Household income for women can fall anywhere from 37 percent to 50 percent after the death of their spouse.

- Upwards of 40 percent of widows report not being confident in their ability to manage finances alone.

- Within 12 months of becoming a widow, 45 percent of women experience a decline in their standard of living.

- Half of all widows lose 50 percent of their household income upon the death of their husband.

- Widows who employ a financial professional before their loss are 90 percent more likely to feel more prepared.

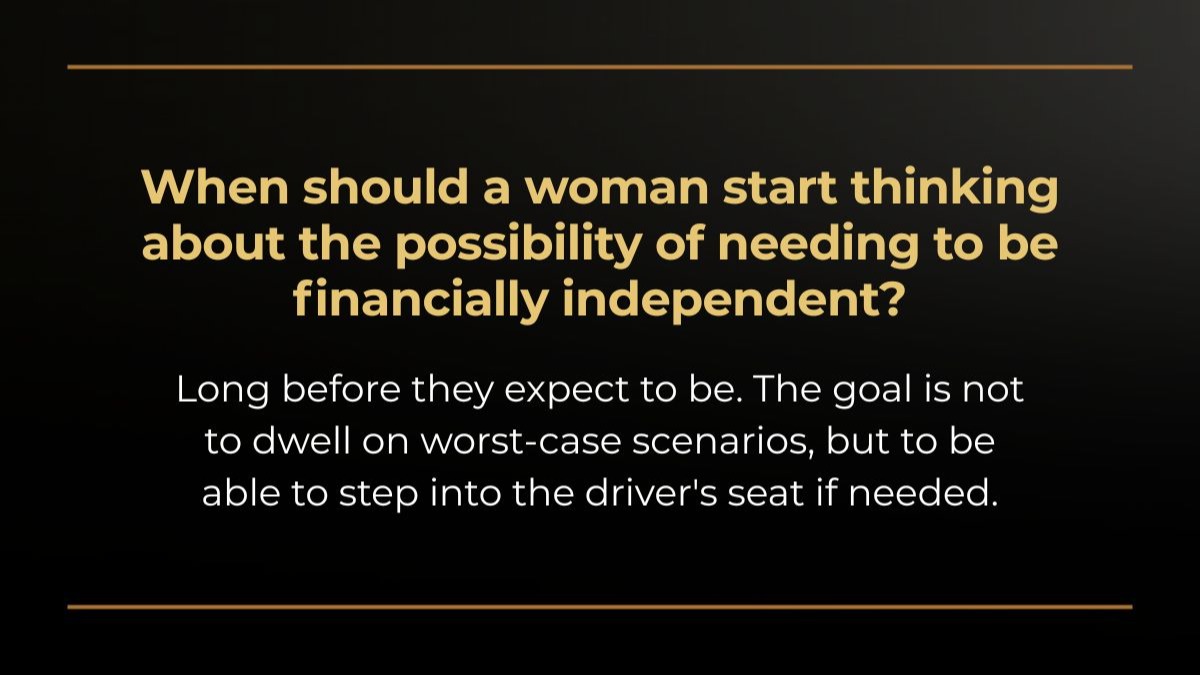

With the average time a woman aged 55 to 64 spends as a widow about 10 years, many women may shift into full financial responsibility earlier than they expect, often while still working or supporting adult children.8

What This Means for a Financial Strategy

If you are a woman in a long-term relationship, these numbers suggest that at some point, you are likely to be the sole decision-maker for family finances, even if your partner handles much of it today. The question is whether you want to learn and organize everything during an emotional time of loss or be ready beforehand.

What Are Three Financial Strategy Moves to Consider?

There are many financial moves women can start making, but we’ve found it helpful for clients to think in terms of three words: clarity, control, continuity.

- Clarity

- Maintain a current inventory of accounts, policies, legal documents, passwords, and key contacts. Check to see if they have up-to-date information.

- Make sure both partners know where this information lives and review it together periodically.

- Control

- Married women should consider being a co-owner, not just a beneficiary, on key accounts where that makes sense.

- Both spouses should understand how their retirement income strategy works, how cash flow is generated, and what is owed to Uncle Sam and how it may change if they become widowed.

- Continuity

- Married women should consider developing a relationship with a financial professional, estate attorney, and CPA, so they are not starting from scratch if they suddenly find themselves as the sole decision-maker. Asking difficult questions can help drive the conversation when their spouse is present.

- Discuss openly with adult children or other individuals you may rely on what the strategy is in the event of widowhood.

Bringing It All Together for Women Who Are Primary or Equal Earners

These three numbers do not exist in isolation. Many women reading this are:

- Earning a share of their family income

- Accumulating assets in their own name

- Likely to outlive a partner and manage wealth on behalf of children and perhaps parents

If This Is Your Current Situation, Here Are a Few Focused Questions to Ask Yourself

- Income protection: If your paycheck stopped for health reasons, could your family maintain its lifestyle and keep savings on track?

- Decision rights: Do your accounts, property titles, and legal documents reflect the role you already play in providing for others?

- Time and energy: Does your financial strategy account for the emotional and practical load you carry, not just the numbers on a spreadsheet?

What Are Some Financial Strategies That May Fit This Reality?

Women who are a primary or equal earner, or are concerned about having to assume full financial responsibility upon the passing of their spouse, may want to:

- Consult with a financial professional to discuss your wealth management and insurance needs.

- Think about building a “career resilience fund.” This is a slightly larger emergency reserve that may provide additional flexibility to change roles, start a business, or take a caregiving break without derailing a long-term strategy.

- Ask a financial professional about account titling. For example, would Joint ownership with rights of survivorship (JTWROS) be appropriate for certain accounts? Also, consider asking about beneficiary designations, and possible use of legal entities in estate considerations.

Why Work With a Financial Professional?

To help translate the three important numbers we’ve discussed into action, you may want to start by reviewing the following questions:

- If my spouse or I live to 95, what does my retirement income strategy look like?

- If a spouse needed to manage finances alone five years from now, what would need to change between now and then?

- How are we preparing for the wealth that may be inherited?

You do not have to figure these out alone. As we saw above, women who use a financial professional before becoming the sole decision-maker are more confident with financial decisions. We are here to help our clients have the confidence to face the future, regardless of what it holds. Please feel free to contact us if you would like to start a discussion.

1 USA Facts, March 21, 2025

2 The Guardian, December 11, 2024

3 McKinsey & Company, May 8, 2025

4 Diversified Trust, October 13, 2025

5 Pew Research Center, April 13, 2023

6 Center for American Progress, May 9, 2025

7 Gitnux, December 11, 2025

8 Resto NYC, October 12, 2023