The Evolving Role of Women in Family Finances

According to a recent survey, 49% of women consider themselves to be the chief financial officer of their households, up from 41% in 2021.1

Those numbers are even more impressive when you consider that until 1974, a married woman often needed her husband’s permission to open a bank account, apply for a credit card, or sign up for a mortgage. Times have changed!2

However, in today’s economic environment, only 64% of women say they feel financially secure—down from 72% in 2021.1

Despite the challenges, there is no turning back the clock on women’s drive toward financial independence and their increasingly important role in their families’ fiscal well-being and the global economy.

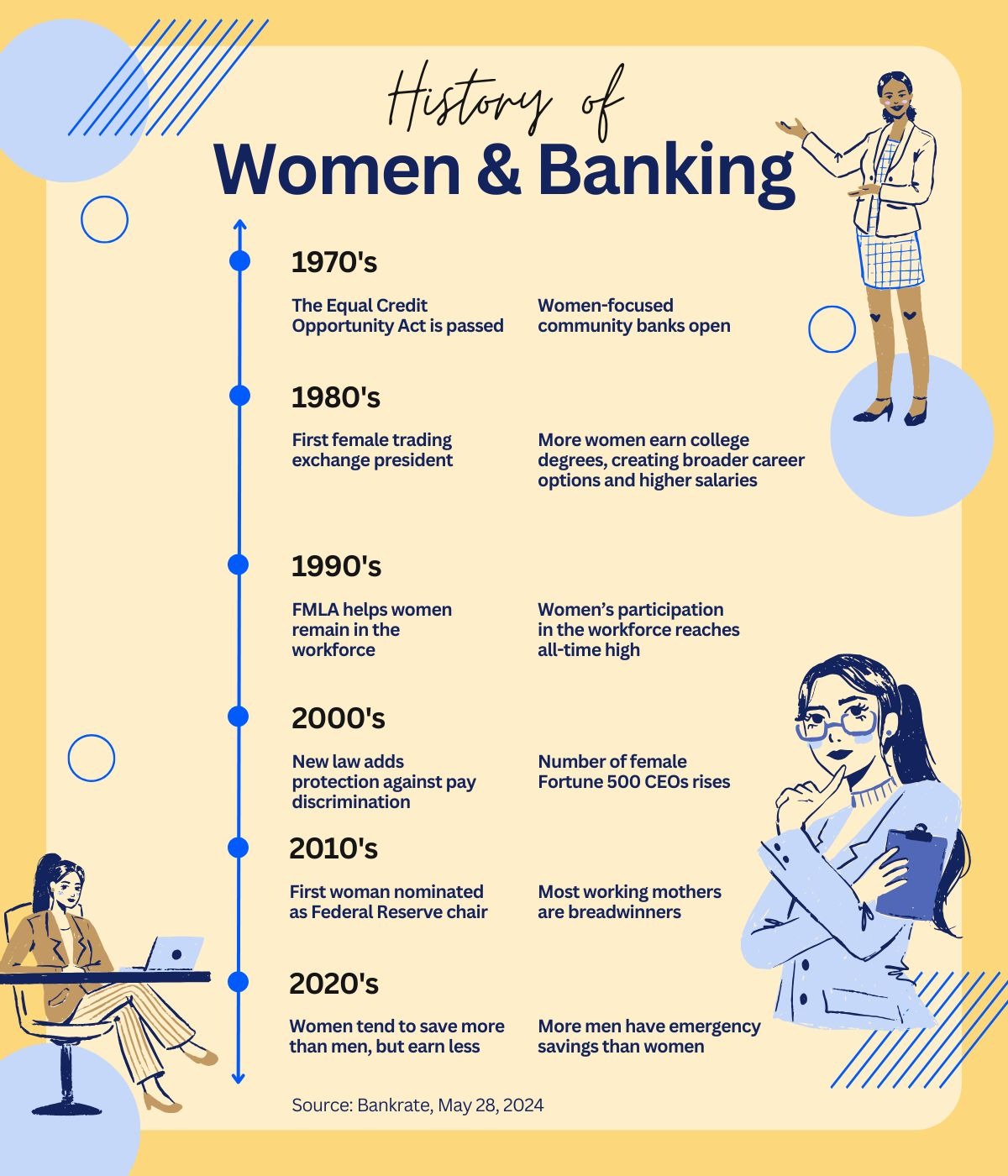

It Wasn’t Always This Way

It may be hard to believe that women had so few financial and banking rights just a few decades ago. While today, more than half of all women are in the workforce, and women can’t be refused credit based on gender, in 1970, only 43% of women were in the labor force, and women could be turned away by lenders if they didn’t have a male co-signer.2

The past 50 years have seen tremendous changes in women’s roles in personal finances. Thanks to hard work, new laws, and regulatory changes, new norms emerged. The chart below highlights some of the milestones that built on each other to reshape gender roles, family dynamics, and society in general.

The Current Landscape

Today, women are financial decision-makers, with nearly 50% taking a lead role in the family regarding money, some by choice, some by necessity. Progress has been made toward accessing credit, investing, pursuing higher education, and having career opportunities. Attitudes have also changed, with the days of women taking a backseat in financial decisions increasingly a thing of the past.

By 2030, women are expected to oversee $34 trillion in the United States, about 38% of all investable assets. That’s almost double from last year and an increase from the $7.3 trillion women controlled just a decade ago. Women are controlling more assets and increasingly becoming the financial heads of households due to several factors, including inheritance, divorce, and career success.3

There are now at least 62 female billionaires and ultra-high-net-worth (UHNW) women–defined as those with $30 million or more–have increased from 6.5% of the UHNW population in 2010 to 11% in 2023.4

As financial professionals, we are focused on meeting women's unique needs and preferences and are committed to building strong relationships with all of our clients.

Women Have a Different Approach to Investing and Family Financial Goals

Our experience has shown that women tend to have different priorities and approaches to investing in and setting financial goals for the family than men.

Here are some ways gender can influence investment decisions:

- Financial Confidence

While many women are confident about their daily financial management skills, some are less confident about investing. For example, one study showed that 75% of women feel confident about balancing a checkbook but only 19% are confident about selecting investments that align with their goals.5

Taken further, while 52% of men say they are confident they are on track with putting money away for retirement, only 42% of women feel that way. It’s no surprise, then, that women tend to be more pessimistic about whether they are accumulating enough assets for retirement.5

- Investment Discipline

Women tend to be more conservative than men regarding the investments they choose. Women are also more conservative about the returns they expect from their portfolios. Avoiding the next “hot” investment may have its rewards.5

- Patience Can Be a Virtue

A Wells Fargo survey showed that women trade 27% less frequently than men. Wells Fargo attributes this to the financial confidence issue, where overconfident investors are more likely to trade frequently, believing they know more than the market. Interestingly, when men share accounts with women, they trade less, even though they tend to take the lead in trading decisions.5

- Managing Market Volatility

We have seen that women are more likely than men to wait out market volatility, and the Fidelity survey backs that up. While 43% of men say they will do nothing and 9% will decrease their investments during market turmoil, 51% of women will wait out the volatility and only 6% will decrease their investments.5

Women are also less likely to use a correction as a “buying opportunity,” with only 16% saying they would increase investments during volatility, compared to 28% of men who would put more money to work.5

- Women Are More Philanthropic

According to Bloomberg, regardless of age or income level, women tend to donate more to philanthropic causes than men. With more money at their disposal, women are likely to give charity in increased numbers.4

- Women Are Comfortable Asking for Directions

Women tend to be more collaborative than men and more open to guidance when it comes to investing. According to Fidelity, 86% of women agree that having their investments managed by a professional makes life less stressful. At the same time, 77% of women believe they would be more confident with the help of a financial professional.5

Finances Can Cause Conflict

Finances can, and often do, cause tension between spouses. Fidelity Investments Couples & Money Study states that nearly 1 in 4 couples say money is their greatest relationship challenge, with 45% of partners saying they argue about money at least occasionally.6

More than 1 in 4 admit to often being frustrated by their partner’s money habits but let it go to keep the peace. The Fidelity study details that 53% disagree on how much savings is needed to retire and 47% disagree on how much risk they are comfortable taking on in their investments.6

In our experience, effective communication is key to managing conflict and helping increase a couples’ chances of financial success. By communicating, couples can discuss their finances, talk honestly about how family money is handled, and agree on short- and long-term goals.

As financial professionals, having both partners involved in setting financial goals and driving discussions can help make client meetings more productive. There doesn’t always need to be agreement, but leveraging each partner’s strengths and listening to their perspectives can help us build consensus and implement financial strategies.

Women Face Challenges and Opportunities

While women’s roles in the workforce and society have evolved significantly over the past few decades, many women still face unique challenges in pursuing financial independence.

Barriers include the gender pay gap, financial education, and lingering societal expectations. While women still earn less than men, they are also more likely to work part-time and take time off throughout their careers to care for children or other family members. Financial independence is also potentially even more critical, given that women typically live an average of five years longer than men.7

As part of the coming “great wealth transfer,” women are expected to inherit much of the $68 trillion in wealth that baby boomers are passing down. Whether husbands are leaving money to their wives or couples are passing a nest egg down to their children, women may benefit disproportionately, and they need to be prepared to handle this influx of wealth.7

Women at all income levels can pursue financial empowerment with the right knowledge, tools, and support.

Building Independent Credit: An Important Step Toward Financial Empowerment

One critical yet often overlooked aspect of financial independence is establishing and maintaining a personal credit history. While it may seem convenient to be listed as an authorized user on a spouse’s credit card, this approach doesn’t offer the same financial security as owning individual credit accounts. Without credit in their own name, women may face challenges when applying for loans, securing housing, or even starting a business.

Opening and managing personal credit cards, responsibly using credit, and maintaining a healthy credit score are steps that may help with long-term financial independence. This proactive approach might also put women in a stronger financial position in the event of major life changes, such as divorce, widowhood, or a spouse’s financial mismanagement. Building independent credit strengthens overall financial resilience and supports greater autonomy in making major financial decisions.

Empowering women to take control of their credit is a foundational step in pursuing lasting financial security and independence.

Working With a Financial Professional

Working with financial professionals can help women on their journeys. Despite the change in attitudes around women’s decision-making regarding finances and investment, some lingering biases can still impact the quality of the services women receive. By being aware of these oftentimes unintentional biases that treat men and women clients differently, you can find a financial professional with whom you can build a strong and trusting relationship.

We should all embrace the opportunities presented by women’s evolving roles in family finances. The contributions women are making are game-changing. At the same time, women must often balance careers, family responsibilities, and financial goals. It’s not always easy. As gender and family dynamics evolve, remember the importance of open communication and collaboration in seeking your family’s financial goals.

Conclusion

No matter who takes the lead in managing finances, thoughtful preparation and collaboration are key to building a long-term strategy. We're here to support you and your family in navigating every stage of your financial journey—helping you become more confident when making decisions that create a lasting legacy for future generations.

1 Allianz Life Insurance Company, February 6, 2024

2 Bankrate, May 28, 2024

3 Financial Advisor Magazine, December 9, 2024

4 Robb Report, December 9, 2024

5 U.S. News & World Report, August 19, 2024

6 Fidelity Investments, February 1, 2024

7 CNBC, December 12, 2023